COVID-19 Update

Dear friends and clients,

We are living in unprecedented times, but we are facing these challenges and uncertainties together. As a business, the Caliber Insurance Brokers team is working to do everything we can to continue to be there for you, providing the high level of service you are accustomed to.

For those of you who currently hold insurance with us, are awaiting a quotation, or are about to get your new policy, we are still here for you and we are taking all the necessary precautions in order to fulfill these duties safely.

With the information we have regarding COVID-19, we are taking the necessary and appropriate steps to keep everyone's health and safety a top priority. One of those steps is to limit contact, as such we have shortened our hours to 10-4, Monday-Friday, and our offices are currently closed to the public as we do our part to encourage social distancing by working 100% remotely.

Through email, phone, or video, we can provide you with updates on current market conditions, rates, and set up action plans to ensure you are receiving all the services you need. Our team has ensured that each one of us has fully equipped home-offices set up to continue serving you, our valued clients, at full capacity.

The health of our clients, our team, and the general public are our highest priority, and we urge you to join us in focusing on the health and safety of our community during these trying times. As per the Government of Canada:

Together, we can slow the spread of COVID-19 by making a conscious effort to keep a physical distance between each other. Social distancing is proven to be one of the most effective ways to reduce the spread of illness during an outbreak.

This means making changes in your everyday routines to minimize close contact with others, including:

- avoiding crowded places and non-essential gatherings

- avoiding common greetings, such as handshakes

- limiting contact with people at higher risk like older adults and those in poor health

- keeping a distance of at least 2 arms-length (approximately 2 metres) from others

Proper hygiene can help reduce the risk of infection or spreading infection to others:

- wash your hands often with soap and water for at least 20 seconds, especially after using the washroom and when preparing food

- use alcohol-based hand sanitizer if soap and water are not available

- when coughing or sneezing:

- cough or sneeze into a tissue or the bend of your arm, not your hand

- dispose of any tissues you have used as soon as possible in a lined waste basket and wash your hands afterwards

- avoid touching your eyes, nose, or mouth with unwashed hands

- clean the following high-touch surfaces frequently with regular household cleaners or diluted bleach (1 part bleach to 9 parts water):

- toys

- toilets

- phones

- electronics

- door handles

- bedside tables

- television remotes

If you are a healthy individual, the use of a mask is not recommended for preventing the spread of COVID-19.

Wearing a mask when you are not ill may give a false sense of security. There is a potential risk of infection with improper mask use and disposal. They also need to be changed frequently.

However, your health care provider may recommend you wear a mask if you are experiencing symptoms of COVID-19 while you are seeking or waiting for care. In this instance, masks are an appropriate part of infection prevention and control measures. The mask acts as a barrier and helps stop the tiny droplets from spreading you when you cough or sneeze.

Most importantly, stay positive and continue to support each other. We can and we will get through this together, growing closer and stronger as a community.

The Caliber Insurance Brokers team is still here to answer any questions you may have, so please don't hesitate to reach out, even if it's just to chat.

You can do this. Take care and stay safe.

-The Caliber Insurance Brokers team

Water Damage: Will Your Policy Leave You High and Dry?

When you think of a home insurance claim, you probably think of fire or theft. While those are dramatic and vivid, its actually water damage that make up half of claims in Alberta.

This post talks about the 5 types of water coverage available:

- Water Escape

- Sewer Back Up

- Overland (Flood)

- Water & Service Lines

- Ground Water

Water Escape

Water escape includes damage from a hot water tank, dishwasher, washing machine or burst pipe. Frozen pipes are a big problem in the winter. It could also include water that gets in from a hail or wind storm – if a tree lands on your house and makes hole, rain can get in.

This coverage is usually part of the main policy.

Sewer Back Up

If you live in the city or an area with sewer lines, these can get filled with water. Too much water in the sewer system can back up into your basement. It’s pretty gross and can be expensive to deal with!

This coverage is optional – make sure you have it! Edmonton sees a lot of sewer back up claims. Even if you don’t have a finished basement, the cost for cleanup and a new furnace can run into the tens of thousands.

We see policies with only $20,000 or $30,000 of coverage. If you have a finished basement, that’s not nearly enough. Ask for a quote on the maximum coverage available.

Overland Water (Flood)

Before the 2013 Calgary flood, no insurance company in Canada covered this damage. Overland water provides coverage if water gets into your home through the front door or the basement window.

Some insurance companies include it with sewer back up and others offer it as an extra. Premiums are about $75 a year. even if you don’t live by a river or lake, we can get flash rainstorms that can cause flooding!

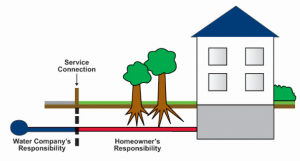

Water & Service Lines

You might see a flyer in your mailbox from the local utility company for this coverage. The water and sewer lines that run between your home and the property line are your responsibility in case they fail, get crushed by a tree root or collapse.

Although not as serious as a sewer back up, it can be a costly hassle. Our insurance companies offer this coverage for about $30 a year. This is a good idea for older homes built in the 1970s or earlier – those lines are more likely to see damage.

Ground Water

Sometimes the soil around your home gets saturated enough for water to actually push through your basement walls. This is considered ground water. The water didn’t come up through the sewer or a window or door.

Some areas around Edmonton collect a lot of water during the Spring melt and that ground water can get into your basement. You’ll notice that your carpet or walls are wet.

When it comes to water coverage, not all insurance policies are the same! We can review your policy to make sure you’re covered.

9 Ways to Save Money on Your Home Insurance

As claims keep going up, so do your home insurance premiums. You can read all about it in our blog post. But is there anything you can do to keep your premiums as low as possible?

Fear not! Here's 9 ways you can save money on your property insurance premiums:

1 - Get a monitored alarm

Professionally monitored alarms are a great way to reduce the risk of theft, fire or water damage. Companies like Sentry and Vivent have alarm systems that can monitor for low temperature, forced entry, fire or water leaks. Insurance companies give the best discount when you have water sensors.

2 - Need a new hot water tank? Go tankless

Hot water tanks normally need to be replaced every 10 years or so. If you’re due for a new tank, think about getting a tankless system. Rather than have a big 40-gallon tube of hot water in your basement, you have a box that goes on the wall. It generates how water on demand, which means the risk of the tank bursting is gone. They’re more expensive, for sure – but a tankless system can save you around $200 a year on your home premium!

3 - Need a new roof? Get Class 4 shingles

If you have an asphalt shingle roof, you need to replace it every 15-20 years. Asphalt shingles are now rated from Class 1 to Class 4. Class 4 shingles are considered hail-resistant and insurance companies give you a nice discount when you have them. If you need a new roof, ask the roofing company for a price on Class 4 hail-resistant shingles.

4 - Doing basement renovations? Get a backwater valve installed

In Edmonton, homes built since the early 1990’s have a backwater valve. It helps prevent a sewer back up during a heavy rainstorm or Spring melting. If your home was built before 1990, chances are it doesn’t have this simple device. If you are doing basement renovations, you’ll have to knock out some concrete to get at the pipe and have one installed. When you do, let your insurance broker know!

5 - Install a Water Flow Device

Intact Insurance now offers a discount when you have a water flow device installed. What’s a water flow device, you ask? It’s a gadget that’s installed on your home’s main water line after the water meter. It monitors a plumping pipes, fittings and appliances for abnormal water flow. If anything is detected, the water is turned off automatically.

6 - Increase your deductible

If you’ve been with the same insurance company for a long time, you still might have a low deductible of $500. A deductible is the amount you pay when there’s a claim. When it comes to home insurance, you want to avoid putting in small claims. Ask your broker to quote your policy with a $1,000 deductible. It will save you money!

7 - Credit consent

Insurance companies now take your credit score into account when quoting. Make sure you give your broker consent to let the insurance company pull your credit history – it can save you a few hundred dollars on your premium! If your credit is good, you will save money. If it isn’t, they won’t count it against you and charge you more.

8 - Avoid small claims

If you have 2 or more claims in 5 years, insurance companies start to really raise your premiums. If we get a bad hailstorm or sewer back up, there’s not much you can do about it – you will have to make a claim. But, if you have some small wind damage and the cost isn’t too high, consider paying for the repairs yourself.

I’ve seen people put in small claims and then something really big happened. Their premiums went up a lot. In some cases, the insurance company declined to renew their coverage! When it comes to claims, pick your battles and get advice from your insurance broker.

9 - Combine your home and auto insurance

If you have auto insurance, you can save a good chunk of money when you combine your home insurance. If there’s ever a claim on both, sometimes you’ll only need to pay 1 deductible. Some companies will even throw in great freebies like free Accident Forgiveness!

[ninja_form id=5]